The Sustainability Committee’s work in 2025 was marked by simplification and burden reduction across the whole reporting and compliance landscape: CSRD, CSDDD, the Taxonomy. The very first attempt of the Commission to create a simplification omnibus had its starting point around these files – and Euromines engaged as a constructive partner to reduce burden and improve conditions for doing business in the EU. At the same time, global developments took off – with the creation of a Standards Based Markets initiative at G7 level and the Critical Minerals Production Alliance that both provide levers to even the level playing field and ensuring access to finance for responsible and resilient projects

Omnibus I

After intense negotiations, our advocacy efforts, targeting several DGs and relevant cabinets of Commissioners, achieved major improvements for our sector under the first omnibus proposal and the final agreement negotiated by the European Parliament and the Council:

- Sector-specific reporting standards for which mining was singled out have been removed.

- Climate Transition Plans are no longer required.

- Scope adjustment: Companies in scope now include those with 1,000 employees and a €450 million turnover threshold, significantly reducing the number of affected entities. Additionally, listed SMEs are excluded from the directive.

- Wave 1 companies: Large companies will not face any additional phase-ins for 2025/2026. Starting in 2027, only the drastically simplified ESRS will apply.

EFRAG on ESRS simplification

Euromines continued to engage with EFRAG, technical advisor to the Commission for sustainability and financial reporting, on the ESRS revision, as EFRAG has been appointed in March to lead on the simplification effort by Commissioner Albuquerque. Euromines participated to the consultation (DL 29/09) asking for a general simplification of the standards and data reporting with specific requests on individual data points.

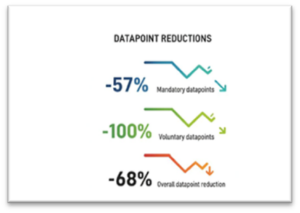

EFRAG’s simplification exercise led to a proposal to the Commission adjusting:

Double Materiality Assessment (DMA):

- Streamlined list of topics no longer mandatory (AR 16).

- Report only material sub-topics.

- Improved aggregation and disaggregation criteria. Clarification that a full DMA is not required annually unless significant changes arise.

- Streamlined list of topics no longer mandatory (AR 16).

- Flexibility to disclose at topic level instead of detailed IROs level when granular reporting is not required

- Reduction of the most granular Minimum Disclosure Requirements (MDRs) under the topical standards and remotion the obligation to justify the absence of Policies, Actions and Targets (PTAs) or to provide timetables for their future adoption, to allow a more concise reporting framework.

- Data point reduction in the topical horizontal standards.

- Better readability and more flexibility to present information by the possibility of including an executive summary at the beginning of the sustainability statement.

- The European Commission is expected to adopt the delegated act by mid-2026. Until then, it will be crucial to closely monitor developments within DG FISMA and other relevant stakeholders to stay ahead of any changes or emerging details.

Euromines actively engages on Standards‑Based Markets, working closely with the OECD as well as with DG TRADE and DG GROW to help drafting a coherent approach in support of a level playing field and increased resilience and transparency of niche-markets to provide tools that help with viability of projects in defence of outpricing practices. Euromines objective is that these initiatives are aligned with the strategic interests of the EU mining sector and ultimately will equip the G7+ (EU, Australia etc.) with tools to ramp up our own raw materials value chains.

On this purpose, Euromines presented a position paper providing input on how a functioning standard-based market for raw materials should focus:

- Guaranteeing access to finance and adequate liquidity.

- Reducing back-end risks for investors, protect from outpricing practices.

- Fostering reliability, price and cost visibility.

- Build trust through more than ESG alone: strong technical requirements, transparent offtake preferences, and credible local‑sourcing commitments all play a key role.

Value Chain Cooperation – a new DG COMP initiative

DG COMP has been working on an initiative to foster cooperation along the value chain to better integrate the demand perspective into existing supply-side policies: after all, without demand, the supply side measures envisaged will not be sufficient to increase the resilience of our value chains.

Euromines stressed that while markets may be functioning, they are not currently operating in Europe’s favour, exposing domestic producers to structural disadvantages. Supply‑side measures alone without a demand perspective is insufficient, so that the set-up requires a more comprehensive industrial policy that considers that global competitors will not reduce production simply because Europe deploys subsidies, premiums, or Buy‑European mechanisms.

Euromines argued that demand integration through cooperation shall eventually lead to a price‑competitive production in the medium term – and must be aligned with the G7 Standards Based Markets initiative. For this, rather than focusing narrowly on each mineral in isolation, the policy approach should centre on the type of industrial ecosystem EU aims to build – and based on this provide a suite of development mechanisms that can be applied in a targeted manner to remedy shortcomings and bottlenecks.

Social and Sectoral Dialogue

Euromines in conjunction with IndustriALL concluded the SODISEES project on 31 October 2025 after two years of collaboration, publishing a report on the importance of social dialogue. The report, “Social Dialogue for Sustainable Extractives Industries in Europe’s” central message: by working together, workers, employers, and public authorities can build stronger industries and secure good, sustainable industrial jobs for the future.

The report outlines concrete measures to strengthen social dialogue and accelerate sustainable practices in Europe’s extractive industries. Please find the completed report here.